Background

Funds paying lifetime and fixed term pensions are required to have annual actuarial certificates. These certificates must show whether there is a high (70%) probability of their being sufficient. These certificates can be used to “segregate” assets into those supporting “current pension liabilities” If assets are not segregated, an annual actuarial certificate is needed to determine the proportion of income that applies to current pension liabilities. This portion is tax free. In addition, the practice can supply certificates prior to pension commencement. For large pension funds, one normally expects a proportion of members to die each year. In small funds, death is “binary” – the member either dies or does not. To allow for this, the practice normally recommends initial pension levels such that if investment and inflation assumptions are realised and no death occurs in the first three years, the 70% certainty will not be breached at the end of those three years.

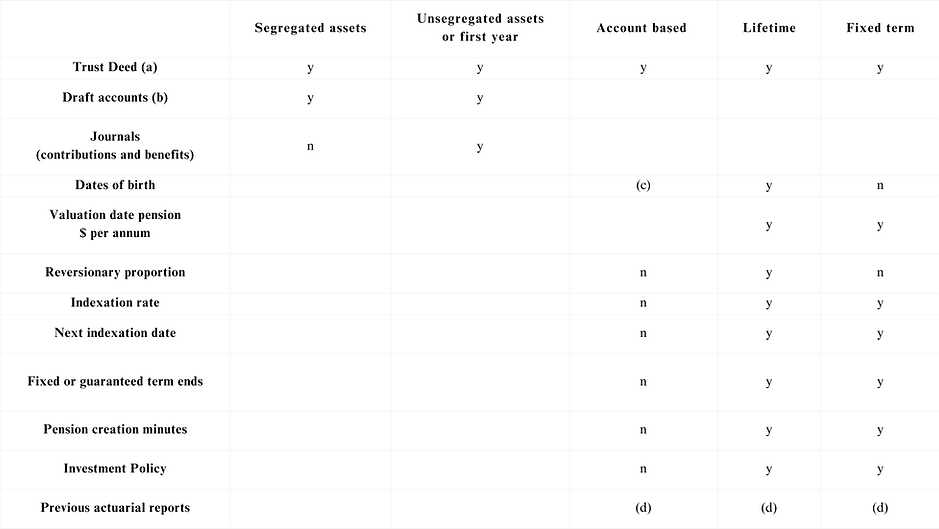

Information needs

The information that the practice usually needs to do any work for self managed superannuation funds depends on the segregation or otherwise of the fund’s assets and the nature of the pensions provided. It includes:

(a) In the case of second or subsequent assignments, a statement to the effect that there has been no change in the trust deed is sufficient.

(b) Year end or commencement of pension.

(c) Only required if certificate of maximum and minimum pension is needed.

(d) Last certificate and (for first review) reports dealing with the creation of pensions.

1.png)

Timing

Certificates are normally produced within five business days of receipt of all information. Urgent tasks will be completed within two business days and attract a 15% surcharge.